UK House Price Predictions 2026: What Buyers and Sellers Need to Know

The UK housing market is entering 2026 with cautious optimism. After a period of economic uncertainty, rising mortgage rates, and the ripple effects of Autumn Budget announcements, the market appears to be steadying — and for many, 2026 could prove to be an ideal time to make a move.

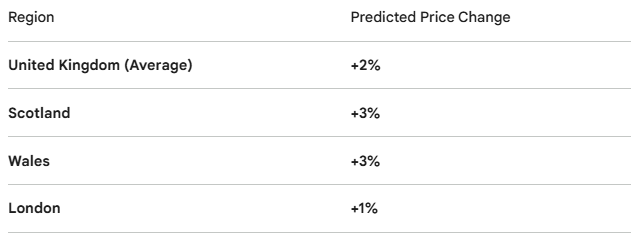

According to Rightmove, new seller asking prices will rise by 2% by the end of 2026. It's a modest but meaningful figure that signals a market finding its footing rather than racing ahead.

What Will Happen to House Prices in 2026?

The headline forecast is a 2% increase in new seller asking prices nationwide. But behind that single number lies a far more nuanced picture, shaped by regional markets, shifting mortgage rates, and government policy changes still working their way through the system.

Buyer affordability is expected to improve throughout the year. Mortgage lenders are exploring ways to loosen lending criteria responsibly, which should give buyers more spending power. Crucially, however, house price growth is expected to remain below average wage growth, meaning homes are becoming more affordable in real terms — a welcome trend, particularly for those saving towards a deposit.

Regional House Price Predictions for 2026

One of the defining features of the 2026 market, according to Rightmove, is how dramatically it will vary by location. The north-south divide looks set to widen further:

Rightmove forecasts that Scotland, Wales, and northern England will outperform the national average. Better affordability, stronger demand relative to supply, and lower exposure to stamp duty changes all contribute to a healthier outlook in these regions.

London and the south of England, by contrast, face a more subdued year. According to Rightmove, these areas are still absorbing the impact of stamp duty changes that came into effect in April 2025, and the looming mansion tax (due to take effect in 2028) is already beginning to cast a shadow over the top end of the capital's market.

How the Economy Will Shape House Prices

Interest rates and mortgages

The Bank of England's Base Rate now sits at 3.75% heading into 2026 — lower than in recent years and a significant factor in improving affordability. According to Rightmove, markets are anticipating at least one further rate cut this year, with a roughly 50/50 chance of a second later in the year.

A lower-than-expected inflation reading could trigger further reductions in early 2026, Rightmove suggests, particularly affecting two-year fixed-rate products. Notably, two-year fixed rates overtook five-year rates as the cheaper option in 2025 — the first time that has happened since autumn 2022 — and that gap is expected to widen further throughout the year.

Inflation and wages

As inflation continues to stabilise, Rightmove points to improving conditions for sustainable — rather than volatile — house price growth. With wages expected to grow faster than property prices, the balance between earnings and housing costs is gradually shifting in buyers' favour.

What Does 2026 Look Like for First-Time Buyers?

According to Rightmove, 2026 shapes up to be one of the better years in recent memory for those looking to get onto the property ladder. Several favourable conditions are converging at once:

- More homes on the market, giving buyers greater choice and negotiating power

- Wage growth outpacing house price inflation, improving long-term affordability

- Mortgage rates lower than in 2023, 2024, and 2025, reducing monthly repayment costs

- Lenders loosening Loan-to-Income ratios, potentially allowing buyers to borrow more

That said, Rightmove acknowledges that challenges remain. Many first-time buyers will still need family support to reach their deposit, and mortgage rates — while falling — remain significantly higher than those seen at the start of the decade.

For those who are ready to act, 2026 is shaping up to be a genuine buyer's market with good availability and room to negotiate. Use the Fraser & Co Tools and Calculators to work out your budget, estimate stamp duty costs, and plan your next move with confidence.

The Mansion Tax and the Top End of the Market

Those with eyes on properties valued above £2 million face a more complex picture. The mansion tax announced in November's Autumn Budget will introduce an annual charge from April 2028:

- Properties valued between £2m–£5m: £2,500 per year

- Properties valued above £5m: £7,500 per year

Though the tax won't take effect until 2028, Rightmove notes that buyer and seller behaviour is already beginning to shift in anticipation. Some sellers may look to price just under the £2 million threshold, while others may seek to reduce their asking price to offset the future annual cost for prospective buyers.

It's worth keeping perspective: according to Rightmove, fewer than 1% of homes in the UK are priced above £2 million, and less than 0.5% of sales take place in this bracket. The impact will be concentrated in London and the south of England, where property values are highest.

Tips for Buyers and Sellers in 2026

For sellers: Price realistically from the outset. With more homes available, buyers have options — and overpriced properties will sit on the market. Research recently sold prices in your area to get a clear view of what your home could achieve.

For buyers: Use this year's buyer-friendly conditions to your advantage. Take time to compare mortgage products and explore what improved Loan-to-Income ratios mean for your budget. Don't be afraid to negotiate — especially in higher-priced areas where demand may be softer. The Fraser & Co Tools and Calculators can help you model affordability and costs before you commit.

For first-time buyers: Prioritise building your deposit and understanding what you can realistically borrow. Use the Fraser & Co Tools and Calculators to run the numbers on mortgage repayments, stamp duty, and overall affordability — so you can plan with confidence ahead of your first purchase.

Those who put their moving plans on hold ahead of the Autumn Budget are now expected to re-enter the market with renewed confidence. This wave of "Budget-pausers" becoming active movers in early 2026 could add meaningful momentum to an already stabilising market.

Planning Your Move in 2026

With modest price growth expected, a good supply of homes, and mortgage rates on a downward trajectory, Rightmove's outlook for 2026 points to real opportunity — particularly for those who have been waiting for the right moment to act. The key is understanding how your local market is behaving and making informed decisions based on current data.

Share this article

More Articles

Sign up for our newsletter

Subscribe to receive the latest property market information to your inbox, full of market knowledge and tips for your home.

You may unsubscribe at any time. See our Privacy Policy.